Suppressed Volatility

As I stated, during a "bullish advance," investors become incredibly complacent. That "complacency" leads to excessive speculative risk-taking. We see clear evidence of that activity in various "risk-on" asset classes from Cryptocurrencies, to SPAC's, to "Meme Stocks."

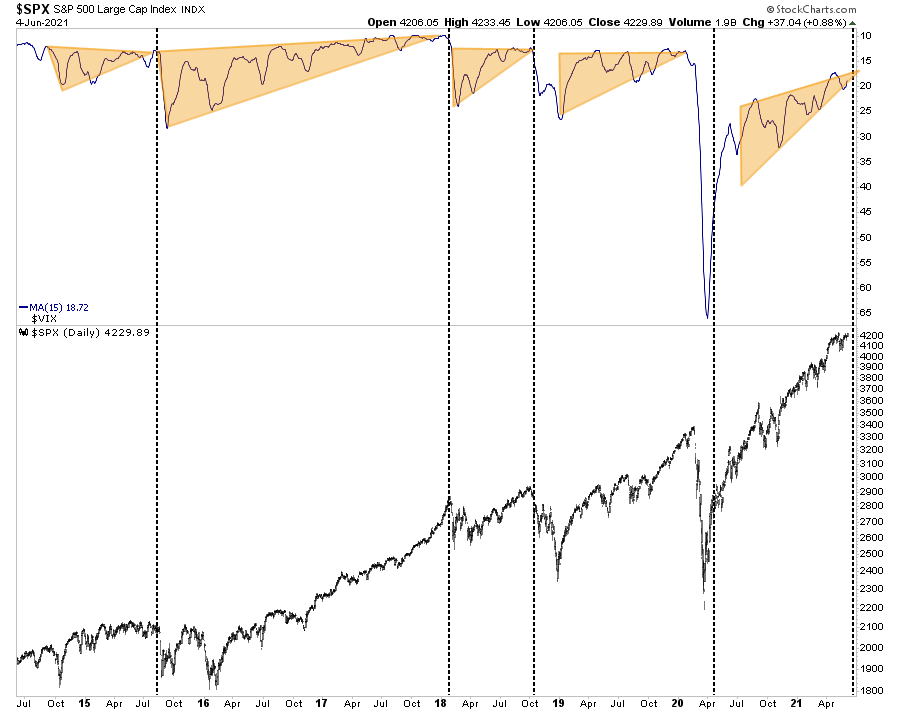

A measure of speculative excess is the Volatility Index (VIX). The chart below is from my colleague Jim Colquitt of Armor ETF's.

The top pane is the 15-day moving average of VIX, which is on an inverted scale. The bottom pane is the S&P 500 index.

"The market may have one last push higher over the next several weeks. Such will take the VIX even lower and complete the VIX wedge pattern. That pattern has been evident in the last three 10% or greater corrections. By this measure, the correction should begin somewhere around July 21st – August 10th." – Jim Colquitt

As they say, "timing is everything." While a July-August time frame is entirely possible, a June-July correction is just as likely. What is essential, as we will discuss momentarily, is understanding that risk is prevalent.

Market Exuberance Stretched Again

It isn't just complacency that is suggestive of a short-term market correction. There are numerous others as well.

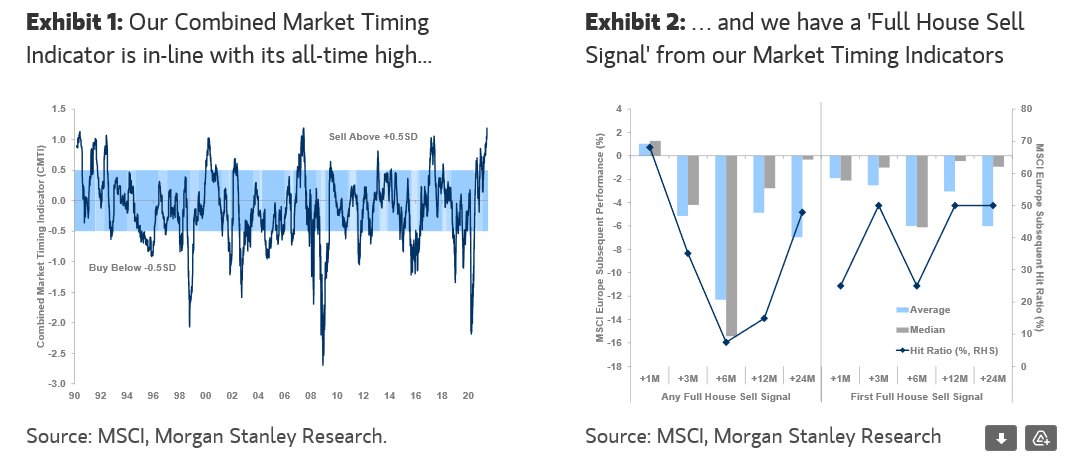

As my friend Daniel Lacalle recently posted, Morgan Stanley's market timing indicator is at levels that have typically coincided with market downturns. Just for reference, the current reading is the most "bearish" on record.

Furthermore, a host of other indicators posted by @Not_Jim_Cramer also suggests there are reasons for concern about a correction.

No comments:

Post a Comment