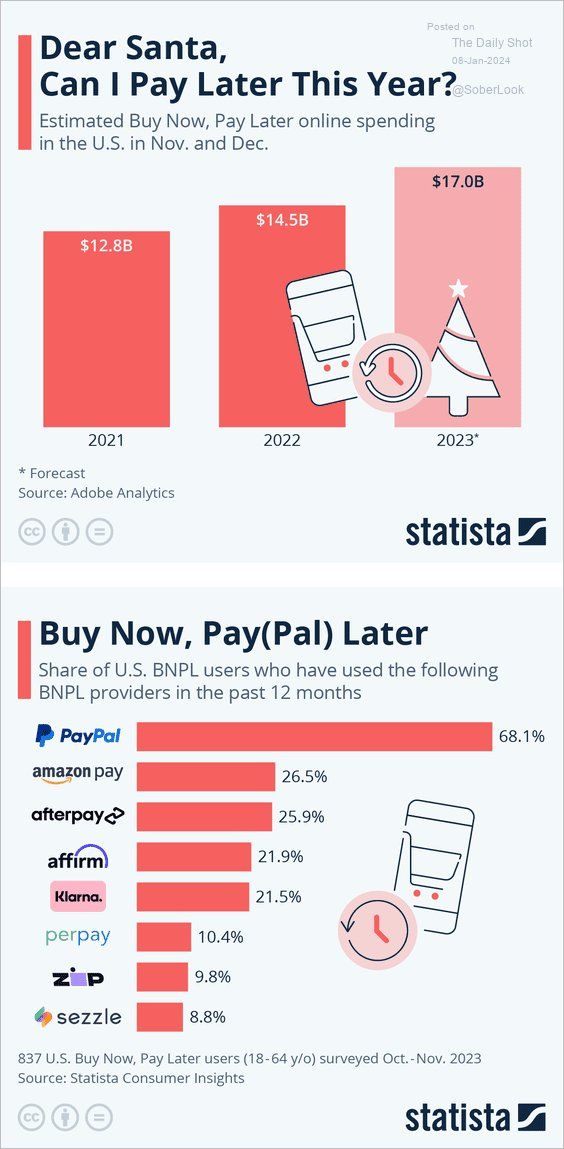

Since 2022, credit card debt has grown 10% annually to a record high of $1.08 trillion. That is double the growth rate prevailing before the pandemic. As banks tighten lending standards and an increasing number of credit card holders max out their cards, some consumers are turning to buy now, pay later loans. Buy now, pay later loans are a little different than credit cards. Unlike credit cards, consumers pay some of the purchase price at checkout. Further, they agree to a series of payment installments. Often, the loan is paid off in three months. Buy now pay later loans typically do not charge interest unless payments are delinquent. Late or rescheduled payments can be costly, typically around 25% of the purchase value. The Statista graphs below show that the amount of buy now pay later loans is relatively small but growing quickly.

The economy continues to hum, but the growth of buy now pay later loans leads us to believe that many individuals, especially lower-income consumers, are in poor financial shape. Per the St. Louis Fed, the credit card delinquency rate is now 3%. Such has been rising steadily since troughing at a record low in 2021. Not only has it turned up and trending higher, but 3% is the highest rate since 2012. The proliferation of consumer credit is not necessarily a problem today. However, if unemployment rises, consumer credit will falter and pressure bank profits and ability to lend. The other factor to consider is that buy now pay later borrowers are now paying off their Christmas purchases and, therefore, consuming less. Such will weigh on economic activity over the next few months.

Lance Roberts

No comments:

Post a Comment