Inflation Is Surging

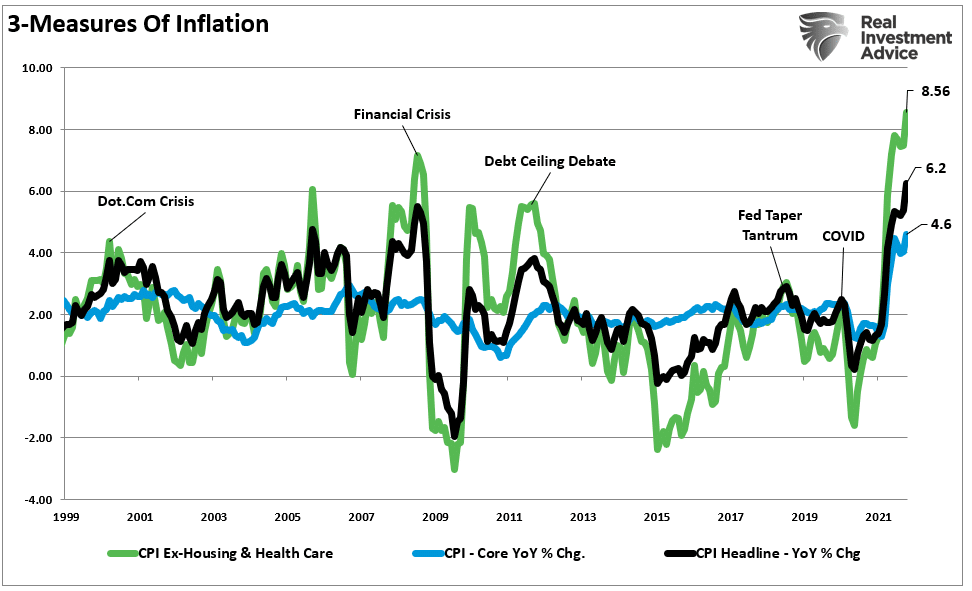

On Wednesday, the latest print of the consumer price index came in much hotter than expected. The chart below shows 3-measures of inflation:

- CPI

- Core-CPI (Less food and energy,) and

- Variable-CPI (Less healthcare and rent.)

The surge in inflationary pressures is evident, with "Core CPI" surging to 6.2% on an annualized basis. However, for most Americans, their food and energy consumption is something they deal with every week. Therefore, the impact on discretionary incomes is far more insidious when those get included.

As my colleague Doug Kass noted:

"My eyeballs tell me inflation is running a fair bit hotter than what is being reported now. I think the average person would also think that based on their buying experiences today."

Furthermore, most individuals have their rent or mortgage payments under a contractual agreement for a certain period. The same goes for healthcare costs as premiums stay stable under a contractual term. The "Variable CPI" shows what inflation looks like from a consumer's point of view. At 8.5%, it is not surprising consumers are getting upset.

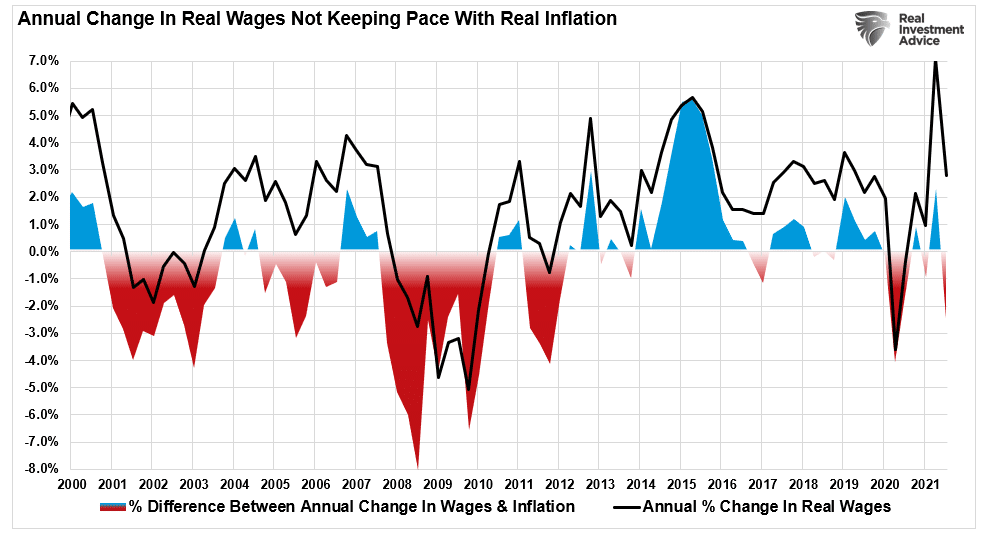

Consequently, the surge in variable CPI is even more problematic when wages fail to keep up with inflationary pressures. Therefore, despite headlines of rising wage pressures, real wages are currently 2% below the annual pace of inflation. So, again, the implications on economic growth, and the market, are not tremendous.

The Fed Has To Be Sweating

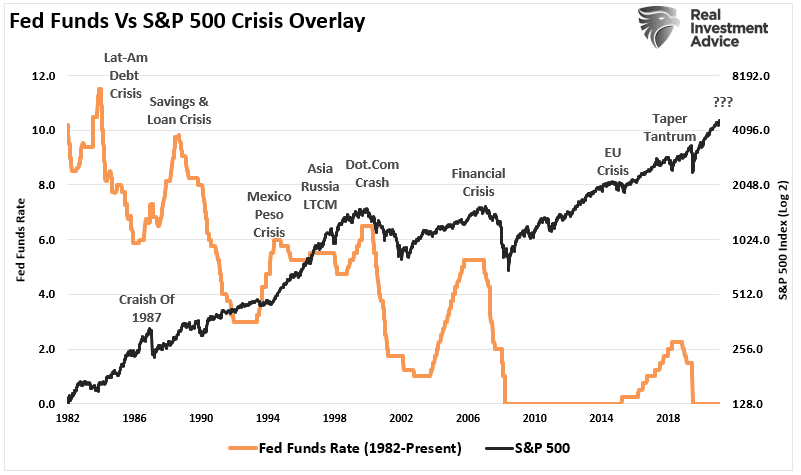

As discussed in "Did The Fed Set The Market Up For A Crash," the choice of ignoring inflation in hopes of getting back to historically low unemployment rates may be problematic.

"Ignoring the inflation risk is likely unwise. Previous spikes in the inflation spread aligned with weaker economic growth, stock market contractions, or crashes."

When it comes to 'full" employment, Michael Lebowitzran some analysis suggesting the Fed may be overly confident in its abilities to support economic growth.

"The U6 Unemployment Rate is not as well followed as the U3 shown above. U6 includes those unemployed in the U3 number but also those underemployed and discouraged from seeking jobs. Jerome Powell thinks the U6 figure is a more credible indicator given the pandemic-related dislocations. As shown below, the U6 rate is 0.4% below the average of the five years leading to the pandemic."

As Michael concludes, the Fed has already met its mandate of full employment. However, they are ignoring inflation to support asset valuations that the Fed recently admitted were excessive.

"Prices of risky assets keep rising, making them more susceptible to perilous crashes if the economy takes a turn for the worse. Asset prices remain vulnerable to significant declines should investor risk sentiment deteriorate, progress on containing the virus disappoint, or the economic recovery stalls." – Bloomberg

Ignoring the surging rates of inflation to support asset prices may result in a "policy mistake" that leads to the one outcome the Fed is trying to avoid – a stock market crash.

Of course, such would not be the first time the Fed's hubris exceeded their grasp and led to unwanted outcomes.

It is likely to be no different this time.

However, I am sure the Fed is starting to sweat.

No comments:

Post a Comment