Sunday, September 29, 2013

Hope you have got Yahoo already

Yahoo (YHOO) is on fire these days, trading over $33 now. It has a gigantic stock holding of the Chinese eBay, Alibaba, which is going IPO. Alibaba's IPO market cap is estimated over $15 Billion. You can image how much the Yahoo investors are excited about this. I started to talk about investing in Yahoo early 2012 (first here, followed by here and here). Hope you have got in. As you may know me, I did get in but with options. At that time, my cost for the Yahoo calls was $1.13 per share. Now it was trading at $13.60 last Friday. In other words, my positions have shot up over 1000% in less than 2 years. Talking about the power of the option trading! (See the chart below). But don't chase it if you want to get in now. I think YHOO is a bit parabolic, which never ends well in the short term. I will continue to hold my positions but will not buy it at this moment. If you want to buy, you will likely get a better price later. Be patient!

How to become millionaire with one boring stock

Not many people understand the power of dividend compounding. When you talk to people about investing in dividend paying stocks, you are often got a funny eye: stupid guy, who on the earth would care about dividend? Go to figure out high flying stocks which can give you a 100% jump overnight. OK, good luck with your dream. Personally, I'm still stubbornly interested in stocks which will pay me increasing dividends and hold them forever. To me, this is a sure way to get rich with very little risk and almost no additional work. Give you an example here.

I know I will get laughed at when I mention Microsoft (MSFT). What the heck to even think about this dead & boring stock! Well, I know it is boring but it can really make you rich, as long as you have the patience. MSFT is a cash gusher and a great dividend payer. There is a good blog on MSFT's dividends. As you can see, it has a great track record of increasing dividends year after year: 5 year dividend growth rate at 15.3% & 10 year dividend growth rate at 28.4%. Let's use the low end of a 15% dividend growth rate for the next 20 years. If you buy 1000 share today at $32 and reinvest all the dividends for 20 years, what will happen? Well, a simple $32,000 at the outset will lead you to a millionaire without you doing anything else. Simply watching and waiting. Is it amazing? That's why the greatest scientist, Albert Einstein, called compound interest – interest on interest – the eighth wonder of the world.

Note how much dividend you will ultimately earn if you simply reinvest it over the time, over $1 million vs just $131,000 if you don't compound it. The thing is, for investing in good companies with increasing dividends, you don't need to look for the stock to go up. Actually you will be better off if the stock goes down, since your dividends can buy more shares when they are reinvested, which will lead to bigger and bigger dividend earnings. That's the sure way to make you rich. Try to understand this concept if you haven't got it.

I know I will get laughed at when I mention Microsoft (MSFT). What the heck to even think about this dead & boring stock! Well, I know it is boring but it can really make you rich, as long as you have the patience. MSFT is a cash gusher and a great dividend payer. There is a good blog on MSFT's dividends. As you can see, it has a great track record of increasing dividends year after year: 5 year dividend growth rate at 15.3% & 10 year dividend growth rate at 28.4%. Let's use the low end of a 15% dividend growth rate for the next 20 years. If you buy 1000 share today at $32 and reinvest all the dividends for 20 years, what will happen? Well, a simple $32,000 at the outset will lead you to a millionaire without you doing anything else. Simply watching and waiting. Is it amazing? That's why the greatest scientist, Albert Einstein, called compound interest – interest on interest – the eighth wonder of the world.

Note how much dividend you will ultimately earn if you simply reinvest it over the time, over $1 million vs just $131,000 if you don't compound it. The thing is, for investing in good companies with increasing dividends, you don't need to look for the stock to go up. Actually you will be better off if the stock goes down, since your dividends can buy more shares when they are reinvested, which will lead to bigger and bigger dividend earnings. That's the sure way to make you rich. Try to understand this concept if you haven't got it.

Saturday, September 28, 2013

Why is Bernanke scared

If you are following my blog closely, you should not be too much surprised by the latest no action decision by the Fed. In the contrast, the whole world seems to be shocked by Bernanke's this decision. Everyone called it unexpected and unprepared. Really? Just a few weeks ago, I said: In the short term it could be very volatile. If indeed the 10 year Treasury moves up to 3%, Bernanke will be scared to death and likely the Fed will do something to calm down the market. This is exactly what has happened: The Treasury quickly approached the critical threshold of 3% prior to the Sep Fed meeting. Bernanke got terrified, and he retreated from his earlier promise to tapering the QE and decided to calm down the market by not tapering. In his post-FOMC press conference, Bernanke acknowledged that he was concerned about the fast increasing bond rate that would impede the recovering housing market. So what will happen next?

Well, the Treasury rate has since plunged to around 2.63% from 3% within days after the Fed meeting. This is a huge move in such a short timeframe. But I think it will continue to move downward toward the level of 2.5%. This is great news for people who are doing financing with a mortgage that is very sensitive to the Treasury rate. Indeed the mortgage rate is coming down substantially as well these days. I'm glad as I'm waiting for a closing of a house in a couple of months. If you are also looking for a mortgage, take the opportunity as I don't think this historical low rate will last too long. As soon as another hint of tapering QE emerging, the Treasury will be moonshooting again. Ultimately, the bond market will do what it wants to do regardless: to move high, much much much higher lasting for decades!

So I repeat my idea one more time: if the Treasury rate drops to 2.5% again, start to build up positions with shorting long-term bonds. One simple way to do so is to buy the inverse ETF: TBF. This could a huge winning position for decades long. Don't ignore it!

Well, the Treasury rate has since plunged to around 2.63% from 3% within days after the Fed meeting. This is a huge move in such a short timeframe. But I think it will continue to move downward toward the level of 2.5%. This is great news for people who are doing financing with a mortgage that is very sensitive to the Treasury rate. Indeed the mortgage rate is coming down substantially as well these days. I'm glad as I'm waiting for a closing of a house in a couple of months. If you are also looking for a mortgage, take the opportunity as I don't think this historical low rate will last too long. As soon as another hint of tapering QE emerging, the Treasury will be moonshooting again. Ultimately, the bond market will do what it wants to do regardless: to move high, much much much higher lasting for decades!

So I repeat my idea one more time: if the Treasury rate drops to 2.5% again, start to build up positions with shorting long-term bonds. One simple way to do so is to buy the inverse ETF: TBF. This could a huge winning position for decades long. Don't ignore it!

Sunday, September 22, 2013

How to bite Apple

Well, Apple is behaving exactly as what I have expected for it: it came down from the recent high of over $500 to touch $450 in the past few days. As I said, anywhere between $440-460 is a good buy for Apple. We got it and I think it is the time to bite Apple!

There are many ways to bite Apple and it is tasty anyway. But at the high level, there are basically two ways to bite it:

There are many ways to bite Apple and it is tasty anyway. But at the high level, there are basically two ways to bite it:

- Buy Apple and hold it for your retirement with dividend reinvestment. Apple is fundamentally cheap with a great value and you don't need to worry about its capability to pay your dividend. The dividend will only get bigger and bigger. This is a worry free trade: you buy it and then simply forget it. Ten years from now, suddenly you will find you have a created a big amount of money for your retirement, which will become bigger and bigger as long as you hold it. The day to day volatility of its prices is simply a noise. Just ignore!! I have already had Apple in my retirement portfolio and I just add more.

- The other way to bite Apple requires a bit technical skills. If you know how to trade with options, there is a great way to buy Apple with a super discount and unlimited upside. If you sell a LEAP Apple put option in combination with buying a LEAP call option, you will basically create an Apple position equivalent to as low as below $400. Yes, you heard me right. I can easily shoot for Apple at around $380 that I'll not loose a penny unless it plunges over $80 from the current level. And I can enjoy all the upside potential, regardless how high it wants to go. I'm excited about this trade, especially with this great value play. You don't often get this kind of opportunity.

Friday, September 20, 2013

Zero risk with unlimited upside

Probably no one will believe that there is such a deal that has ZERO risk but unlimited upside potential! But here is: Everbank creates a new CD again for emerging market currencies: Colombian peso, Indian rupee, Mexican peso, and Turkish lira. With a minimal $1500 deposit for 5 years, you will enjoy at least 15% or more (uncapped) profit if the currencies' performance is positive at expiration or you get all your money back (the worst scenario). Your principle is FDIC insured up to $250,000. You cannot get a safer deal than this.

Emerging markets have just gone through rather depressing period of time and their currencies are also performing very poorly in the past year. But this actually becomes a sweat spot for anyone interested in this CD because the upside for such currencies is more than the downside risk. In other words, the chance of earning 15% or more is much higher than simply getting back the principle. I personally had a very good and profitable experience with an Everbank CD with a similar term but for gold. If it sounds interesting, you should check it out. It will be closed by Oct 9.

Emerging markets have just gone through rather depressing period of time and their currencies are also performing very poorly in the past year. But this actually becomes a sweat spot for anyone interested in this CD because the upside for such currencies is more than the downside risk. In other words, the chance of earning 15% or more is much higher than simply getting back the principle. I personally had a very good and profitable experience with an Everbank CD with a similar term but for gold. If it sounds interesting, you should check it out. It will be closed by Oct 9.

Sunday, September 15, 2013

Will Boston Scientific continue to stay on its own?

About 18 months ago I talked about Boston Scientific Corp (BSX) and thought it was a good value stock at around $7. I'm wrong till now as it has not been acquired yet but does it really matter? Since then, BSX has jumped up 100% and is approaching its 5 year high around $13. As you can see below, I bought BSX call options in Apr 2012 at $0.38 for 20 contracts (equivalent to 2000 shares), which is now worth $2.23 per share. So the option profit is 455% as of now while the stock price has been "just" 100% more. This also shows why options are much better for investment if they are used correctly. I have sold 5 contracts to book in some money that is more than my original cost; in other words, I'm guaranteed to make some money in this trading. So the remaining 15 contracts will be my house free money which I intend to keep and let it ride. I think there is much more upside movement ahead for BSX.

|

2.23 | 15 | $0.38 | $2,669.30* | 455.75% |

Here are a few bright spots for BSX, which makes me continue to be bullish on it. I also think there is still a good chance that BSX may be acquired by J&J or others.

- BSX recently reported solid 2nd quarter results and based on the encouraging numbers, it raised its 2013 revenues and EPS guidance. BSX has solidly turned around.

- BSX got a new FDA approval for its IntellaTip MiFi XP catheter

- BSX has expanded its electrophysiology (EP) offerings with FDA approval of its IntellaTip MiFi(TM) XP catheter and 510(k) clearance of its Zurpaz(TM) 8.5F steerable sheath, which has become a first-line treatment approach for patients with certain kinds of irregular heartbeats.

- To further stengthen its EP business, BSX has announced its plan to acquire Bard EP, the EP business of C.R. Bard, for $275 million. The acquisition is expected to close in the second half of 2013.

- BSX has also expanded its business footprint into emerging markets, especially China and India. It will invest approximately $150 million in China over the next 5 years to build a local manufacturing operation. This will further enhance its profit margin.

Friday, September 13, 2013

Preferred stock for natural gas

For those of you who are not familiar with preferred shares, they are like a mix of a stock and a bond. The share price can fluctuate but is typically not as volatile as the price of common stock. Still got confused? Well, let's put that way. Buying common stocks, you are the owner of the company; as such you can enjoy the growth of the company via dividends and stock capital gains. But if you buy bonds or preferred stocks of a company, you the lending the money (lender) to the company; as such you are not interested in whether the company is doing good or bad, which is nothing to do with you. You are only interested in getting the money back plus interests. So the company is legally bound to pay you the agreed interests as priority if you buy their bonds or preferred stocks (PS). Even better, if a company skip their interest payment due to whatever reasons, it must pay back the missed amount when it resume its payment later. So when you buy PS, don't expect to see too much price appreciation but you can usually enjoy a much higher interests from it. Your aim is to get income from it. Since PS usually don't fluctuate much in price (but it will still change to a much smaller extent), adding some PS in your portfolio may help reduce the volatility of your overall portfolio. PS is usually issued at a price of $25 per share. Since it is traded also in the open market, it can still move around this price. Of course, it is better to buy below $25 if you are lucky.

So nowadays what is the good place to buy PS? Oil and Gas companies! US is undergoing a revolutionary breakthrough in this field. It has drastically reduced reliance in foreign oil and is in the process to export natural gas. It is expected that the US may become oil/gas independent completely within the next 10 years or so and may even become a major oil/gas exporter! This is a huge long term megatrend, which you don't want to miss! Anyway, the PS I'm talking about today is Goodrich Petroleum Series D Cumulative Preferred Stock (NYSE: GDP-D). The yield is 9.75%, $0.609375 per share on a quarterly basis.

Similar to bonds, companies can redeem the preferred shares at a set price on a certain date. For this preferred stock, the company can redeem them at $25 per share on August 19, 2018. In other words,

you should be able to enjoy approximately10% annual income for at least 5 years. Even better, the D shares are currently trading just below the $25 price. So you will get a bit more if the shares are redeemed at $25.

Please note, that various brokers and websites list preferred ticker symbols differently. For example, Etrade lists it as GDP.PR.D and it is currently trading at $24.96.

So nowadays what is the good place to buy PS? Oil and Gas companies! US is undergoing a revolutionary breakthrough in this field. It has drastically reduced reliance in foreign oil and is in the process to export natural gas. It is expected that the US may become oil/gas independent completely within the next 10 years or so and may even become a major oil/gas exporter! This is a huge long term megatrend, which you don't want to miss! Anyway, the PS I'm talking about today is Goodrich Petroleum Series D Cumulative Preferred Stock (NYSE: GDP-D). The yield is 9.75%, $0.609375 per share on a quarterly basis.

Similar to bonds, companies can redeem the preferred shares at a set price on a certain date. For this preferred stock, the company can redeem them at $25 per share on August 19, 2018. In other words,

you should be able to enjoy approximately10% annual income for at least 5 years. Even better, the D shares are currently trading just below the $25 price. So you will get a bit more if the shares are redeemed at $25.

Please note, that various brokers and websites list preferred ticker symbols differently. For example, Etrade lists it as GDP.PR.D and it is currently trading at $24.96.

Wednesday, September 11, 2013

Update on Apple

Yesterday was the day that Apple announced its new iPhones and today Apple got crashed by over 5% today, just as I predicted that people simply sell the news! Apple is changing hands around $467, close to my targeted "bottom" of around $450. Technically speaking, $460 is its first support line and $440 is a second strong support line. I think anything between the two should be a good spot to get in. Warm yourself up if you want to step in.

Sunday, September 8, 2013

Make money while drinking soda

Probably everyone knows Coca-Cola (KO) or Pepsi. They get rich, super rich by selling soft drinks. Actually people around the world are addicted to soft drinks, which will never change and continue so forever! That's why you can become very rich by simply holding KO shares with reinvestment of its dividends for long time, even if KO stock itself is not going anywhere. This is how Buffett has becomes so rich. Well, now you may also invest in another type of soft drink company, which appears to be an emerging star in the soda industry. I'm talking about SodaStream International (SODA).

SodaStream develops, manufactures, and sells home beverage carbonation systems that enable consumers to transform ordinary tap water instantly into carbonated soft drinks and sparkling water. Nowadays, people love DIY, Do It Yourself. You see, you can buy modern style of furniture from IKEA to put things together tailored to your personal taste. You want to select additional features for a new car you want to buy to meet your own interest. You love the DVR programming function on your cable TV to watch whatever and when you want...... I can go on and on. This is the trend, a huge trend that people simply want their own way of doing things or to have everything personalized as much as possible. It is the same thing about what and how to drink soda water. SodaStream catches the opportunity and is revolutionizing the way soda is made. With SODA's system you can have complete control over the contents and flavor of your soda. This has become a huge business now. SODA has reported very strong earning results and is predicting year-over-year revenue and net income growth of 25% and 18% for 2013. Not only its business in the US is growing quickly, it has also expand its sales in Asia and Western Europe. SODA is also doing more partnerships to further strengthen its business. Recently it announced that it will work with Whirlpool Corp for a joint effort aimed to develop a carbonation system that will carry the KitchenAid brand. Another huge potential for SODA that not many people are talking about is that, with its increasingly successful business model, the chance of it being acquired will substantially increases.

SODA has come down from its high recently. If the general market tumbles, SODA may go down further. It will be a great buying opportunity for this young company with huge potential. It will likely to be the next generation of Coca-Cola, if it is not bought out by KO eventually.

SodaStream develops, manufactures, and sells home beverage carbonation systems that enable consumers to transform ordinary tap water instantly into carbonated soft drinks and sparkling water. Nowadays, people love DIY, Do It Yourself. You see, you can buy modern style of furniture from IKEA to put things together tailored to your personal taste. You want to select additional features for a new car you want to buy to meet your own interest. You love the DVR programming function on your cable TV to watch whatever and when you want...... I can go on and on. This is the trend, a huge trend that people simply want their own way of doing things or to have everything personalized as much as possible. It is the same thing about what and how to drink soda water. SodaStream catches the opportunity and is revolutionizing the way soda is made. With SODA's system you can have complete control over the contents and flavor of your soda. This has become a huge business now. SODA has reported very strong earning results and is predicting year-over-year revenue and net income growth of 25% and 18% for 2013. Not only its business in the US is growing quickly, it has also expand its sales in Asia and Western Europe. SODA is also doing more partnerships to further strengthen its business. Recently it announced that it will work with Whirlpool Corp for a joint effort aimed to develop a carbonation system that will carry the KitchenAid brand. Another huge potential for SODA that not many people are talking about is that, with its increasingly successful business model, the chance of it being acquired will substantially increases.

SODA has come down from its high recently. If the general market tumbles, SODA may go down further. It will be a great buying opportunity for this young company with huge potential. It will likely to be the next generation of Coca-Cola, if it is not bought out by KO eventually.

Be ready to buy Apple again

Since I predicted that Apple could be on fire a few weeks ago, Apple has already made some explosive move. I thought it moved up too fast too soon and expected that it could soften towards around $450 as the next big move. Apple is going to announce its next generation iPhone on Tue, Sep 10. News also broke out that Apple will announce a discounted iPhone for China to tap on the huge smartphone market, for which it has not yet been successful. Usually this kind of good news should pop up the share price but it didn't. This is likely a sign that any good news is not new anymore for investors as it has been priced in. I think people may more likely to behavior as "buying the rumors and selling the news". I expect Apple will be batted badly in the very near term, which will create a great buying opportunity for it.

Saturday, September 7, 2013

When nobody wants, you should buy

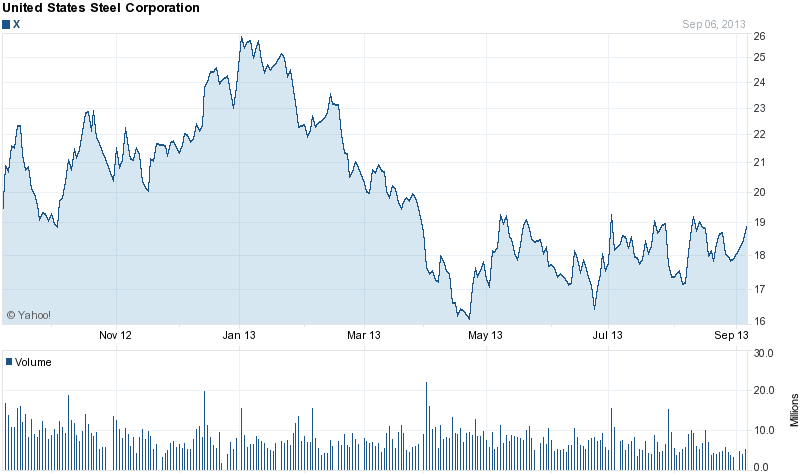

If I ask you which sector is among the most hated and poorly performed in the past few years, can you tell me? Yes, precious metals are one of them. As I said a few weeks ago, I think precious metals may be turning around. Anything else? Well, that's right, STEEL! The steel industry initially recovered along with the overall market after the US credit crisis in 2009. But the EU debt crisis hit it really hard and since 2011 this sector has never come out of the woods. Of course understandably no one wants to buy steel if the industries using steel are all in the water: housing, car, infrastructure construction etc.

The thing is, the biggest and easiest money is usually made when everyone hates something but the situation becomes a little bit better than expected. I think steel is right at this moment. You see, the economy, even though is still struggling, is slowly improving, even in the Eurozone. The emerging markets, especially China, is also slowly improving. You likely have heard all kind of stories regarding the recovery of the US housing market although I'm not sure we are totally out of the woods yet. In a nutshell, I think the demand for steel will be increasing. It is estimated that the steel price will increase by 3% next year. With this kind of super depressed mode in this sector, a little bit good news may probably make it jump by 20-30%. Actually it seems some early sign of uptrend has already emerged. See United States Steel Corporation (X). I start to establish some positions in steel.

The thing is, the biggest and easiest money is usually made when everyone hates something but the situation becomes a little bit better than expected. I think steel is right at this moment. You see, the economy, even though is still struggling, is slowly improving, even in the Eurozone. The emerging markets, especially China, is also slowly improving. You likely have heard all kind of stories regarding the recovery of the US housing market although I'm not sure we are totally out of the woods yet. In a nutshell, I think the demand for steel will be increasing. It is estimated that the steel price will increase by 3% next year. With this kind of super depressed mode in this sector, a little bit good news may probably make it jump by 20-30%. Actually it seems some early sign of uptrend has already emerged. See United States Steel Corporation (X). I start to establish some positions in steel.

Monday, September 2, 2013

How to play oil now?

I'm not interested in politics at all but like or not, our life will be impacted by political decisions directly or indirectly. The current oil market is an example. Crude oil is near &110 these days. It is way too high if considering fundamentals. So why can it be so much inflated? Well, Syria is the major reason for people to become hype for oil. Yes, if Syria is going to get military attacks, for sure oil will be kept high for some time. But the thing is, when a crisis is coming, the price for the relevant goods is usually going up and factored in prior to the moment when the crisis actually happens. Quite often, when the crisis really occurs, the inflated price will soon come down, especially if the price is not supported by the fundamentals. I think this will likely turn out to be the situation for oil. As long as the expectation that Syria will be attacked is out there, the oil price will continue to be high and may even go further higher. However, when the attack to Syria finally breaks out, I bet the oil price will soon plunge.

If you are interested to play with the crude oil, here is what I will suggest: buy the bullish ETF for oil for now such as the leveraged ETF, UCO. But as soon as Syria gets attacked, sell UCO immediately and buy SCO, a bearish leveraged EFT for crude oil. Of course, this is only a short term speculation. But in the longer term, I think the crude oil will go down substantially.

If you are interested to play with the crude oil, here is what I will suggest: buy the bullish ETF for oil for now such as the leveraged ETF, UCO. But as soon as Syria gets attacked, sell UCO immediately and buy SCO, a bearish leveraged EFT for crude oil. Of course, this is only a short term speculation. But in the longer term, I think the crude oil will go down substantially.

Subscribe to:

Posts (Atom)