Friday, May 31, 2013

Shorting Tesla?

Tesla Motors (TSLA) is a company that designs, develops, manufactures, and sells electric vehicles and electric vehicle powertrain components. All the sudden, TSLA has become the Wall Street darling. TSLA has advanced almost 100% in the past 2 weeks (see below). It is definitely parabolic! Whenever something becomes parabolic, it will end badly with no exception!! So it is time to short TSLA? Not necessarily so. Shorting anything is not an easy job, especially when everyone wants to short. TSLA is probably among those stocks which have the highest shorting interest these days. There are 40% positions shorting TSLA. If TSLA refuses to immediately go down but rather goes up for a while, there will be a so-called short squeeze: those shorting it on margin will be forced to cover by buying back the stocks, which will further propel the popping up of the stock price. While it is very tempting to short TSLA, I'm not brave enough to do so at the moment. But I did notice that TSLA dropped hard today by 7%. It will be fun to see how TSLA will go in the next few weeks. If it jumps back and becomes more parabolic, then it may be a good time to short it.

Thursday, May 30, 2013

Buy more NLY or AGNC now

Along with hard selling of mREITs including NLY and AGNC in the past week or so, the discount to their book value for both NLY and AGNC is around 9-10%. It is a clear over-reaction, which creates a great buying opportunity if you want to establish a postion or add more. The more it is sold, the less risk it will have. You just need the gut and patience to do so. Simply buying NLY or AGNC will give you a yield of 12% or 18% respectively as it stands now. And a good chance of great capital returns in the months ahead. If you really want to have safety, then using cover call to generate more income to protect your capital. If you go deep enough into the money when writing a call, you may almost completely protect your capital while enjoying the high yield. I know it is very technical but for those who understand options, this is some food for thought.

Monday, May 27, 2013

Along with the shorting master to go short for Seagate?

If you haven't heard about Chanos, you need to know him. You must know the fate of Enron, the big energy-trading company that went broke in 2001. Before anyone in the Wall Street knew it, Chanos already knew that Enron would go bankrupt and he went ahead to short it. The result? He got a huge profit by shorting Enron. Of course, he did not stop there. He went on shorting big of WorldCom, Dell, Hewlett-Packard, and Petrobras etc and all of them were big winners for him. It is not overstating that Chanos is the godfather in identifying and shorting troublesome companies!

So what is Chanos' target now? Well, one of Chanos' top ideas for shorting now is Seagate Technology (STX). STX main business is computer hard drives. This is kind of obsolete business when more and more people are moving towards "cloud" memory. Chanos is betting that STX will suffer when people use more mobile devices using different kinds of memory or cloud services instead of local hard drives.

STX stock has advanced over 4 times in the past 2 years, from $8 to now around $40. So there is a big ditch for STX to tip over, if Chanos is right and usually he is right.

So what is Chanos' target now? Well, one of Chanos' top ideas for shorting now is Seagate Technology (STX). STX main business is computer hard drives. This is kind of obsolete business when more and more people are moving towards "cloud" memory. Chanos is betting that STX will suffer when people use more mobile devices using different kinds of memory or cloud services instead of local hard drives.

STX stock has advanced over 4 times in the past 2 years, from $8 to now around $40. So there is a big ditch for STX to tip over, if Chanos is right and usually he is right.

Sunday, May 19, 2013

Opportunity is coming again for NLY and AGNC

Unfortunately I will be extremely busy moving forward in the rest of the year and I'm not sure if I can continue to write as regularly and often as in the past. I will try my best but likely will be more sporadic and less detailed. Hope I can still give your some thoughts on opportunities as far as I can in a timely fashion.

Not sure if you have noticed these days that AGNC and NLY were both hit very hard. Well, this could be another good opportunity for buying them, if you not yet having them at all, or adding more shares to your existing positions. The idea is to buy them when they are trading substantially below their book value. Right now, here is the what they stand:

AGNC book value $28.94, current price $29.65

NLY book value $15.19, current price $15.01

AGNC is still a bit above its book value but NLY is slightly below its book value. While my gut feeling is to expect both of them may go further down before stabilizing, there is no sure thing on this. Buying some at this price is not a bad idea although not a supper great deal. Dollar-averaging is always a better idea in such an uncertain period, i.e. buy a bit now and buy more if it declines more.

Not sure if you have noticed these days that AGNC and NLY were both hit very hard. Well, this could be another good opportunity for buying them, if you not yet having them at all, or adding more shares to your existing positions. The idea is to buy them when they are trading substantially below their book value. Right now, here is the what they stand:

AGNC book value $28.94, current price $29.65

NLY book value $15.19, current price $15.01

AGNC is still a bit above its book value but NLY is slightly below its book value. While my gut feeling is to expect both of them may go further down before stabilizing, there is no sure thing on this. Buying some at this price is not a bad idea although not a supper great deal. Dollar-averaging is always a better idea in such an uncertain period, i.e. buy a bit now and buy more if it declines more.

Saturday, May 11, 2013

European stocks have better valuation

A few days ago, Buffett told CNBC that his company was buying European stocks. He said Europe "is going to be around" and its economic problems present a buying opportunity. Well, if you really want to find some opportunity to put your money into work now, it is not a bad idea to follow Buffett's footprint. The US stocks have relentlessly climbed up for half a year without any meaningful pause, which is very unusual. While I don't know when, the time will come that the rug is suddenly pulled out from underneath. There is no exception. Although from the historical perspective the US stocks are not yet supper expensive, they are quite pricey at a PE of 16 times in average. It would be much better to buy US stocks if they drop 10-15% from the current level. However, the European stocks are much cheaper, trading just 12 times this year's earnings. That's 20% cheaper than the US stocks. Of course, Europe is facing a lot of significant economic problems but as Buffett said, such problems actually bring a buying opportunity, given their stocks are relatively cheaper. Actually in the past year, the European stocks have been doing much better than the US stocks. If you compare the European 50 blue chips included in the index ETF, Euro Stoxx 50 (FEZ), against the S&P 500, FEZ is clearly outperforming S&P 500 (26% vs 22%). This trend will likely continue, barring any disasters occurring in the Europe.

Friday, May 10, 2013

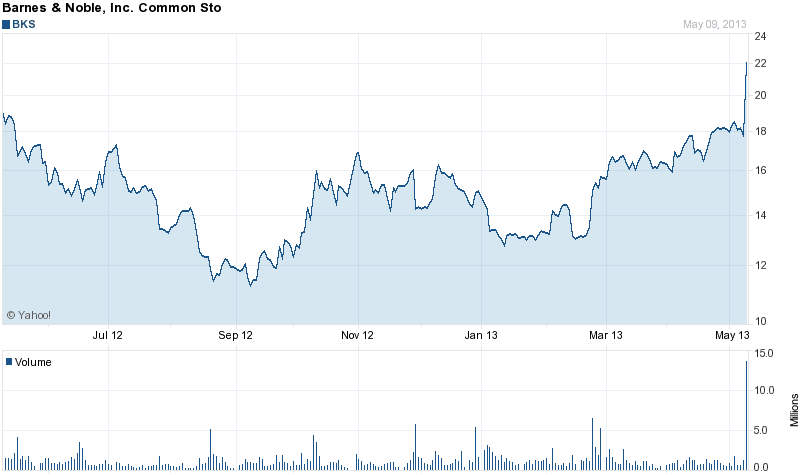

Have you bought Barnes & Noble?

Barnes & Noble (BKS) in on fire these days, especially in the past 2 days that it shot up almost 30%. What happened? Well, rumors surfaced 2 days ago that Microsoft could buy the bookstore chain's Nook

business, the division of Barnes & Noble responsible for

making e-readers and tablet devices, with a price tag of $1 Billion. This is obviously huge positive news for BKS. Back in Sep 2012 I thought BKS was a hidden gem with a great valuation when it was trading hands at around $13. If you got in then, you should be really happy with a 77% jump from this position a little bit over 6 months. While in the long-term, I think BKS will still go up probably another 50% from here, in the short-term, I'm not so sure. At the end of the day, it is still a rumor and there is no guarantee that this deal is real and if so, will go through. A sharp decline will ensue if the deal does not materialize. So it is better to either take some chips off the table by taking some profits now or at least keep a very tight stop loss to protect your profits if bad news comes.

Monday, May 6, 2013

Utility stocks are dropping hard today

Just a quick note that utility stocks are among the worst performing stocks for today. While most of the sectors were advancing today, utility stocks dropped 1.35% today. This is a good sign that this sector has indeed peaked and is like to drop further over the next few months. If you are truly considering to short XLU, is it a good time to do so? Purely from the technical point of view, it may likely be much better to wait. Here is why. XLU peaked around $41.44 and now is trading at $40.32. There is a good chance it will try to bounce back to test its resistance around $41 or so. This will technically creat double tops, a bearish charting formation, and that is usually a good spot to initiate a short position. So, I'd wait for a few days to see if this indeed plays out as such before jumping in to start shorting it immediately.

Saturday, May 4, 2013

Utility stocks seem to be parabolic

These days, everyone is hungry for income. When your money only gives you almost nothing by saving them in the bank, people are forced to go somewhere else to look for better income. High dividend stocks have thus become fashion in the stock market to be chased up. One of them is utility stocks. Utility companies such as power or gas companies are a highly regulated sector. In other words, they cannot set the price of power or gas simply by supply or demand but rather any price changes must be approved by the government first. While this sounds negative for utility companies, they are also kind of being protected since it is very difficult for others to step into this industry due to a very high regulatory threshold. In other words, there is not much competition for them. So typically utility companies are highly indebted but pay out high dividend yields, often at 3-4%. With near zero interest rate for savings nowadays, 3-4% dividends are quite attractive and people have poured their money into this sector in the past half a year. Below is the chart for the utility ETF, XLU. It now has come to some extreme to me. Utility companies are typically boring companies. A 25% increase over just 6 months is huge for them. I think it is topping now for utilities, especially considering May is usually a bearish month for stock markets. People usually say "Sell May and go away". If you own utility stocks, at least you need to be careful to monitor them and lock your profit timely without giving back too much. If you don't own them, definitely not a time to buy now. I'm even considering to short XLU for the next few months.

Subscribe to:

Comments (Atom)