Jeremy Grantham recently made headlines with his latest market outlook titled "Let The Wild Rumpus Begin." The crux of the article gets summed up in the following paragraph.

"All 2-sigma equity bubbles in developed countries have broken back to trend. But before they did, a handful went on to become superbubbles of 3-sigma or greater: in the U.S. in 1929 and 2000 and in Japan in 1989. There were also superbubbles in housing in the U.S. in 2006 and Japan in 1989. All five of these superbubbles corrected all the way back to trend with much greater and longer pain than average.

Today in the U.S. we are in the fourth superbubble of the last hundred years."

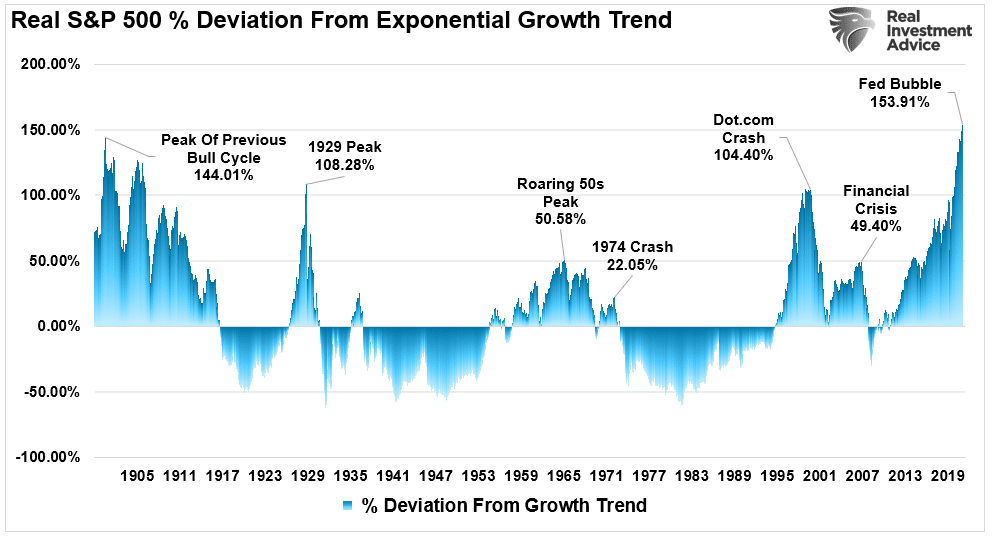

The bubble is easy to spot in the chart below of deviations of the market from its long-term exponential growth trend.

As Grantham correctly notes, investors don't want to admit that a correction of magnitude is possible. However, the possibility of a 40-50% contraction to revert the massive extension from the long-term growth trend is highly probable. All that is needed is a catalyst, which so far has yet to appear.

Could the Fed be the catalyst? Maybe.

The problem is that crashes start slowly and then all at once. Only in hindsight does the catalyst become obvious.

No comments:

Post a Comment