In 2018, Gary Gensler was but a humble professor at MIT, lecturing about a fringe topic: cryptocurrencies.

With conviction, he declared, “In terms of market value, probably three-quarters of this space has already been determined by the Securities and Exchange Commission not to be a security… So about three-quarters of the market value right now is what one might call cash, or a commodity, but not a security in this world.”

Oh, how the times have changed.

Since ascending to the throne of the SEC, Gensler's tune has taken a peculiar twist. A twist so pronounced that one might not even be able to call it a twist. Maybe a twirl. Or perhaps even a convolution.

In an about-face, Gensler quickly insisted that most cryptocurrencies are securities.

Yet even then, Gensler remained steadfast in a singular message: the SEC is resolutely technology-neutral. Our sacred duty is to safeguard the innocent lambs of the investing world.

What he told Bloomberg in 2021 would be repeated over and over in the mainstream media…

He said:

“While I’m neutral on the technology, even intrigued—I spent three years teaching it, leaning into it—I’m not neutral about investor protection. If somebody wants to speculate, that’s their choice, but we have a role as a nation to protect those investors against fraud.”

The SEC, he said, acknowledges the importance of being open to innovation but emphasizes the need for a regulatory framework to ensure the protection of investors.

That was Dr. Jekyll.

Amenable. Gracious. Here to help.

But slowly, over time, we began to see a different side of our affable academic:

Mr. Hyde.

“Come in and Register”

As you probably know…

The U.S. Securities and Exchange Commission (SEC) has filed a lawsuit against Coinbase, alleging the popular cryptocurrency exchange failed to register as a securities exchange.

Are we shocked? No.

The SEC's lawsuit follows a Wells notice issued to Coinbase six weeks prior, indicating the SEC's intent to recommend enforcement action against the company.

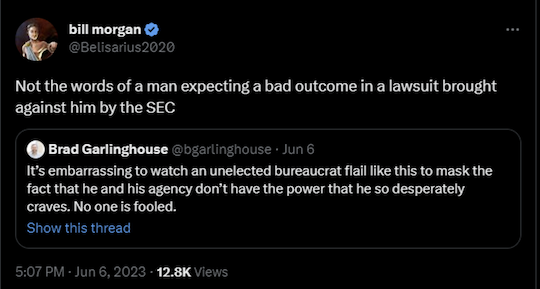

As a result, Coinbase's stock (COIN) has dropped 14% on the week.

Strangely, Paul Grewal, Chief Legal Officer of Coinbase, expressed a sense of relief upon receiving the lawsuit from the SEC. Coinbase has been seeking clarity from the SEC for years, he said, making the legal action somewhat of a welcome development.

"Finally,” he said, “I now at least know what it is that we are accused of.”

Grewal argues that Coinbase had been operating in the dark, with the SEC refusing to reveal which products and services were under scrutiny. He says that the SEC’s constant call for crypto companies to “come in and register” has been disingenuous at best.

“As things currently stand today,” he said, “no operating exchange or other intermediary can register with the SEC. There’s no way for issuers to practically register under the current regime.”

Worse, when crypto companies try to do so in good faith, they are made targets by enforcement actions.

No comments:

Post a Comment