By Trish Regan

I wonder who's pumping Jerome Powell's gas...

Because it's clearly been a while since the Fed chairman pulled up to a pump himself...

Speaking to lawmakers in a congressional hearing last month, the Fed chairman doubled down on his view that there is no real inflation in the U.S. economy.

"I graduated from college in 1975," Powell told lawmakers. "I had a front-row seat," he said, referring to the devastating inflation that plagued the U.S. economy during the Carter years... "I don't expect anything like that to happen," he said, adding that the double-digit price increases of the 1970s would be "very, very unlikely."

Powell explained that recent inflation has everything to do with "this unique historical event that none of us has lived through before" and nothing to do with inflation spiraling out of control. And this is the reason he's watching employment measurements instead of inflation measurements to determine when we need to raise rates and when we need to scale back on his $120 billion per month bond-purchasing extravaganza.

You got to give Powell points for his consistency, if nothing else... He repeatedly keeps telling us that this inflation is just temporary.

It's amazing how wedded our central bankers can become to a particular viewpoint. It may be this conviction to a belief system (in this case "no inflation") that causes them to repeatedly fail the American public by over or underreacting in almost every economic challenge.

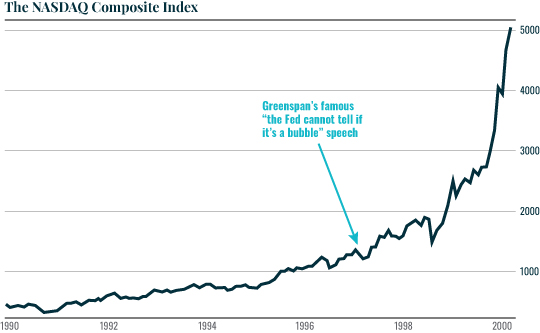

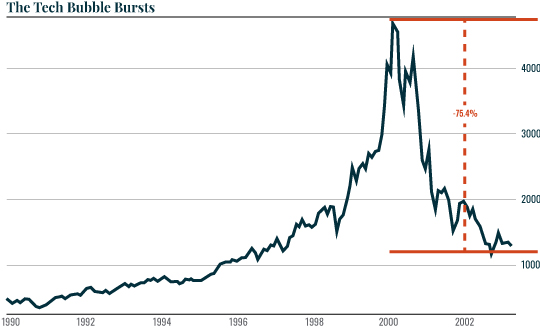

For example, former Fed Chairman Alan Greenspan was late to loosen rates ahead of the disaster that became the systemic financial crisis of 2008. This inaction exacerbated the problem. Overly generous liquidity in the prior years left interest rates too low for too long, creating an easy money environment that led to overly aggressive lending strategies. When the time came that the Fed needed to cut rates... it didn't have much room to lower them. So, it moved too cautiously...

And on the plus side, since this current mess began unfolding in March 2020, the Fed has done an excellent job stepping up to the plate in a major way. It lowered rates and began a liquidity program by purchasing bonds, thereby helping to keep rates low. In sum, the Fed – along with multiple rounds of coronavirus stimulus checks and generous unemployment packages – helped to mitigate a full-on economic crisis that could have, if left unchecked, devastated the economy for years to come.

A round of applause is in order... a standing ovation, even.

But now, it's time for everyone to sit down.

The coronavirus crisis in the U.S. has come and gone. We fought the war with COVID-19, and we won. The economy has reopened and "help wanted" signs are on just about every street corner.

So, why is the Fed still printing money via bond-repurchasing programs and low rates?

It's a fair question and one Powell can't quite answer... Granted, recent Fed minutes suggest they're finally at least willing to discuss tapering off the bond purchases.

But for the most part, Powell and company believe that we need new metrics like employment to gauge the health of the economy.

Let's take him at his word. Let's assume he's right and employment is the only way to truly measure whether the U.S. economy is "back in action." If so, then, even by those metrics... the economy is looking quite healthy.

Last month, we added 850,000 jobs to the American economy and the unemployment rate came in at a healthy 5.9%. Keep in mind that this is despite the lengths that the administration is taking to effectively ensure that those who are unemployed need not go back to work until at least September, when the benefits are set to expire.

The growth of 850,000 jobs in the latest month should be the kind of improvement needed to encourage the Fed to get back into the tightening game before it's too late.

Because, when it's too late... well, it's just too late. We saw that with Greenspan – and I don't know about you, but I'm not in the mood for a repeat of 2008.

Meanwhile, we're seeing real, hard evidence of actual inflationary pressures that you'd think would convince Powell and his team of Fed governors of the need to focus on inflation.

At present, the U.S. economy is facing higher food, higher energy, and higher housing prices. And the prices of most commodities are going up, up, and away...

Food prices are up 2.2% year over year and are expected to move higher. General Mills (GIS), the company that produces giant food brands like Betty Crocker and Cheerios, recently sounded the alarm, telling investors it anticipates inflation of roughly 7% this fiscal year... along with higher input costs including labor and logistics.

Consumer prices on most goods are up 5% annually, according to the most recent read on the Consumer Price Index, and still climbing. (The read on the "core rate", which strips out food and energy is up 3.8%, its sharpest increase in nearly three decades.)

Oil, as I've been predicting, is at $75 per barrel and expected to keep rising.

And this has an effect on prices for everything else. The price of coffee beans, for example, recently escalated because of the shipping costs associated with transporting the beans to their end markets. At the start of June, the futures benchmark in New York for the high-end arabica coffee bean hit a four-and-a-half-year high of almost $1.70 a pound, up almost 70% from a year before.

Yet, despite this reality, the Fed seems quite determined to downplay inflation.

This inflation is just "transitory," Powell tells us. And again, Powell is so not worried that he says he's not even reading the inflation tea leaves, just the employment data.

Is he burying his head in the sand like an ostrich? It certainly seems so.

The reality is this: Inflation is seeping into our economy at such a rate that it would be an economic miracle if the masterminds at the Fed turn out to be correct in calling it transitory.

And Powell isn't the messiah.

The realist in all of us should remember that the Fed has failed, over and over again, to get this right. Instead, it has a tendency to both under and overreact.

In this case, the Fed is underreacting to inflationary pressures. Its refusal to move on both its rates and its aggressive bond-buying programs will have long-lasting effects... courtesy of... (drumroll please) 1970s style inflation.

Consumer and producer prices are all higher, and there are more than 9 million jobs currently open... imagine that!

Is This All Just Lip Service?

Powell and company's dedication to the no-inflation story has turned the old Wall Street bromide of "don't fight the Fed" into "don't trust the Fed."

Take everything you hear from the Federal Reserve with a grain a salt... an inflated one at that.

These academics, thanks to political pressures, have gotten into the poor habit of telling investors exactly what they think investors want to hear.

Think about it... Just a few months ago, it was "We're not raising till 2024." (Who actually thought that was even conceivable?)

Then, when the economic data improved, it was... "We're not raising until the end of 2023."

And then we heard from one Federal Reserve governor talk of 2022.

And now, some Fed governors, including Mary Daly of San Francisco, are pushing to taper in 2021.

So, which is it, guys?

I would bet money the Fed has no idea. But they've got this story of inflation not being a problem, and so far, they're sticking to it.

So, as investors, we need to remain nimble and ready. If the Fed does hike rates in the near future (as a normal, rational person might assume they would, given the positive economic indicators and inflationary reads), then the economy and markets may suffer the consequences.

If they don't raise – and increasingly, the smart money is making that assumption – then the party lives on... until it ends. Badly.

Remember the 1970s inflation? The stock market was a mess. It lost nearly 50% over a 20-month period, and for close to a decade few people wanted anything to do with stocks...

We need more responsible rhetoric from the Fed and even some near-term tapering with a promise to look at all the data in case it needs to move on interest rates. And I believe the market would welcome it.

Is it too much to ask that the Fed review all the data?

That's exactly what Powell should have told Congress in his most recent hearing. He should have said he would remain vigilant and watch all the signals and data points – including employment numbers, producer prices, and consumer prices.

When Janet Yellen was Fed chair, she was good about promising to read all data in real time. So what happened?

Some think that Powell's job might be on the line... and that he's speaking to an audience of one – his former colleague at the Fed, now secretary of the U.S. Treasury, Janet Yellen.

His term is coming up, and some think that she may want to replace him. And, why not? He was "Trump's guy"... liked by former Treasury Secretary Steve Mnuchin, and Powell effectively replaced Yellen herself. As such, she may feel more comfortable putting her own guy, or gal, into the spot. Lael Brainard, a friend of Yellen's, could easily fit the job and might be a preferable and friendly alternative for Yellen.

(Keep in mind, the Yellen we've seen as Treasury secretary is far more aggressive in her desire to tax the world than we ever saw at the Fed... so much so, that she's responsible for the 15% worldwide-tax proposal.)

So, internal politics may also be playing into Powell's positioning – a lousy thought, but nonetheless a potential reality as we try to understand the Fed's backwards thinking.

The bottom line is this... inflation is coming. And at some point, the Fed will need to react.

When that happens, you'll want to be prepared... Capture the momentum on the upside by being invested in markets as they move higher. But you should diversify into some hard assets (gold or real estate). When investors lose confidence in the stock market, they put their capital into these kinds of assets. And you should keep a little cash on hand to be ready to buy some stocks when the pullback in the market happens.

Remember, don't trust the Fed...

Make your own judgments, knowing that sooner or later, the Fed will have to react if only to taper its bond buying, and that – in the long run – it will be healthy for the markets and the economy as a whole.